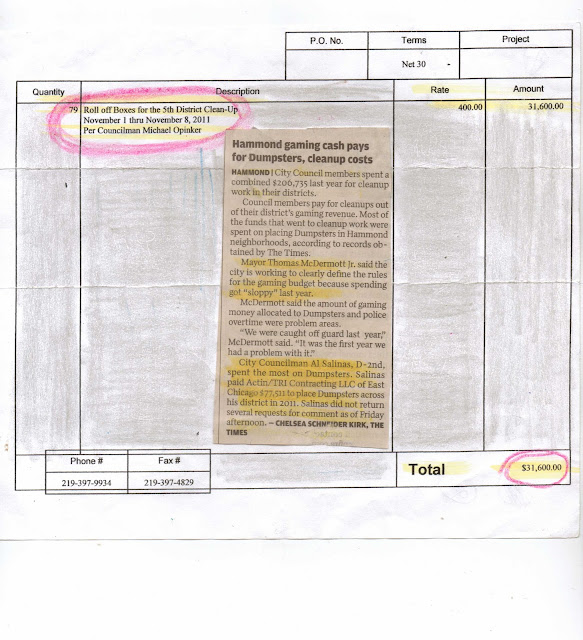

You figure $400 is the going rate for a dumpster. If I'd have ordered 80, I think a volume discount would be called for. Does anyone really know if 80 dumpsters were placed and picked up? Does the city have pick-up receipts/tickets for 80 dumpsters? Or because it's "discretionary" gambling money, is O'Pea's O'kay O'kay to pay? Does the service provider have receipts from where they dumped 80 containers? How many dumpsters are in this contractors inventory? Would O'Pea care if 40 dumpsters were serviced but 80 billed for? Hypothetical..."someone" agrees to overpay, because "someone" isn't paying, "someone else" is. Happens all the time. It is the MO of a majority of kickback routines.

Good point, I was thinking same. If you look at almost any of the State Board of Account Audits on Hammond, they are problematic, with what appears to be poor accounting practices.

As to were 80 dumpsters actually on the street in the district. Could you imagine 80 dumpsters in Opie's District, there wouldn't be enough parking for residents

Hammond, since McDermott arrive appears strife with missing money. Festival of the Lake Parking revenue generated $60,000 at $15 per car give or take a few bucks. For 100,000 people to have arrive in 4,000 cars, it would have been a Ripley's Believe it or not record of 23 people arriving per car?

FINANCIAL REPORT OPINION MODIFICATIONS

The Sanitary District (District) did not provide supporting documentation that management

approved adjusting entries or provide any documentation to support all adjusting entries posted to the

2010 ledger as described further in the comment entitled "Internal Controls Over Financial Transactions."

Therefore, the State Board of Accounts was unable to provide an unqualified opinion on the Independent

Auditors' Report for the financial statements due to insufficient evidential matter.

Accounting records and other public records must be maintained in a manner that will support

accurate financial statements. Anything other than an unqualified opinion on the Independent Auditors'

Report on the financial statements may have adverse financial consequences with the possibility of an

increase in interest rate cost to the taxpayers of the governmental unit. (Accounting and Uniform

Compliance Guidelines Manual for Cities and Towns, Chapter 7)INTERNAL CONTROLS OVER FINANCIAL TRANSACTIONS

The Sanitary District (District) maintains their records on the accrual basis of accounting as

required. As communicated to management during the entrance conference, the financial statements are

management's responsibility. Management also has responsibility for adopting sound accounting policies

and for establishing and maintaining internal controls that will, among other things, initiate, authorize,

record, process, and report transactions (as well as events and conditions) consistent with management's

assertions embodied in the financial statements. The entity's transactions and the related assets, liabilities,

and equity are within the direct knowledge and control of management.

We noted several weaknesses in the internal control system of the District related to financial

transactions.

The District did not have proper internal controls in place in order to provide reasonable

assurance that the financial information and records were in compliance with laws and regulations.

Additionally, proper internal controls were not in place to mitigate the risk of improper activities either due

to error or fraud. We have the following concerns as described below:1. District management was notified in February 2011 that the auditors initiated start of the

audit of the City. Preliminary meetings were held with the City Controller, the Water

Utility executive director, and the District's business manager to review the expectations

of management's completion of their financial presentations. The audit of the District

began on April 18, 2011. At that time, the District had not completed posting all year

end entries in order to present their financial statements in conformity with generally

accepted accounting principles.2. The District continually revised their trial balance during the audit because adjusting

entries continued to be recorded to the ledgers during the course of the audit resulting in

account balances to change. In addition, in November and December 2010, the District

re-opened the 2009 ledger to record audit adjustments after the completion of the 2009

audit. The audit adjustments for 2009 totaled $2,495,919; however, the District

recorded adjustments totaling $6,427,317. The District could not provide sufficient

documentation of the difference in adjustments.3. An entry in the amount of $1,000,000 was recorded to correct the construction in

progress account for the period ending December 31, 2007. However, after our

research of the 2007 records we found that the $1,000,000 was already capitalized by

the District and the $1,000,000 adjusting entry was not necessary. The District

subsequently reversed the adjusting entry.

The arbitrary recording of such transactions

indicates management's lack of expertise or familiarity of historical transactions.

4. A final trial balance, per the financial consultant, was provided to us on May 17, 2011.

We also obtained reports which detailed all the adjusting entries made by the District to

the 2010 ledgers. Adjusting entries totaling $7,010,716 were recorded by the financial

consultant to Company SP6. Company SP6 is the fund that is used to account for the

financial transactions relating to Federal State Revolving Loan Fund. In order to perform

certain audit procedures to determine if the adjusting entries were required, we requested

the District's business manager and financial consultant for the supporting

documentation for the adjusting entries.

We were told by the financial consultant that he

may have some reports to back up the entries but that the descriptions of the entries

were detail enough. Some of the descriptions noted on the adjusting entries were: "to

balance," "adj bal," and "adj entry." Since the adjusting entries could not be audited

because of the lack of sufficient evidential matter to determine if the entries made were

proper, we qualified the Independent Accountant's Opinion.5. The District's ledgers are set up with accounts numbers that aid in the identification of

account types. For example, the 1000 number series of accounts are considered asset

accounts, 2000 number series accounts are receivables, 3000 number series accounts

are equity, 4000 number series accounts are income, and 5000 number series accounts

are expenses. It is common practice that at year end, the income and expense related

accounts are "closed" to the equity accounts.

Historically, the District would expense ongoing improvement projects throughout the

year rather then record the transactions to a construction in progress account. District

officials were instructed that construction in progress account, an asset account, should

to be used to record these transactions in accordance with generally accepted accounting

practice.

The District however, opted to reset certain 5000 expense accounts in the

computer system not close to equity accounts at year end. This unorthodox method

makes it difficult to determine which expense accounts should be capitalized in the construction

in progress accounts or reported as current operating expenses.The District did not reset these 5000 expense accounts in Company R at the end of

2009; therefore, expenses totaling $3,230,630 which should have been capitalized

closed to the equity account. This was not corrected until May 2011.

6. The District recorded additional adjusting entries to cash accounts after the District's

year end bank reconcilements were completed. The District did not update the year end

bank reconcilements to include the adjustments posted to cash accounts. The District's

bank reconcilements did not agree to the ending cash balances per the ledgers.

Between November 2010 and March 2011, the computer system at the Sanitary District

allowed users to issue multiple checks with the same check number. It is evident that

the computer software lacks sufficient controls over the issuing of checks.The District's failure to record 2008 and 2009 audit adjustments to the records in a timely manner

results in management relying on inaccurate information when making financial decisions  .

.This was from the last Sanitary District Audit....

http://www.in.gov/sboa/WebReports/B39221.pdf, page 24-27, The contents of this report were discussed on June 8, 2011, with

Robert Lendi, CPA, Controller; Alan

M. Arendt, CPA, Business Manager; William Biller, Financial Consultant; and Stanley J. Dostatni, President

of the Board of Sanitary Commissioners.

{kind=link}